In reviewing the first wave of reports by 100 large European companies, the study finds that the CSRD has done what it set out to do: push sustainability reporting beyond box-ticking, provide useful data to users and turn it into a genuine management tool for navigating climate and social risks.

Across Europe, companies are beginning to show a more structured and credible approach to sustainability.

- Climate transition planning is becoming a mainstream exercise: 54% of firms now outline such plans and 73% report decarbonisation targets, and a notable 40% committing to net-zero. These commitments are clearly distinguishable from various carbon neutrality commitments.

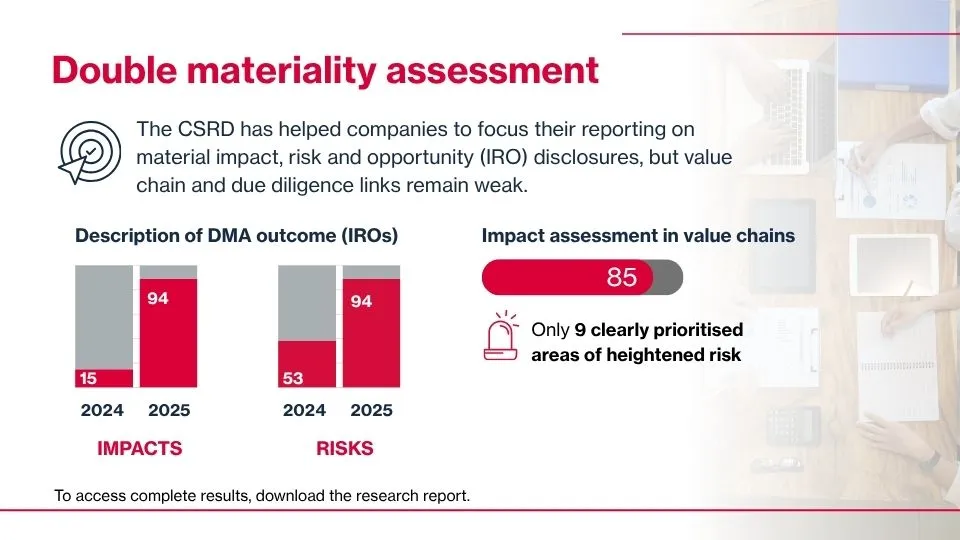

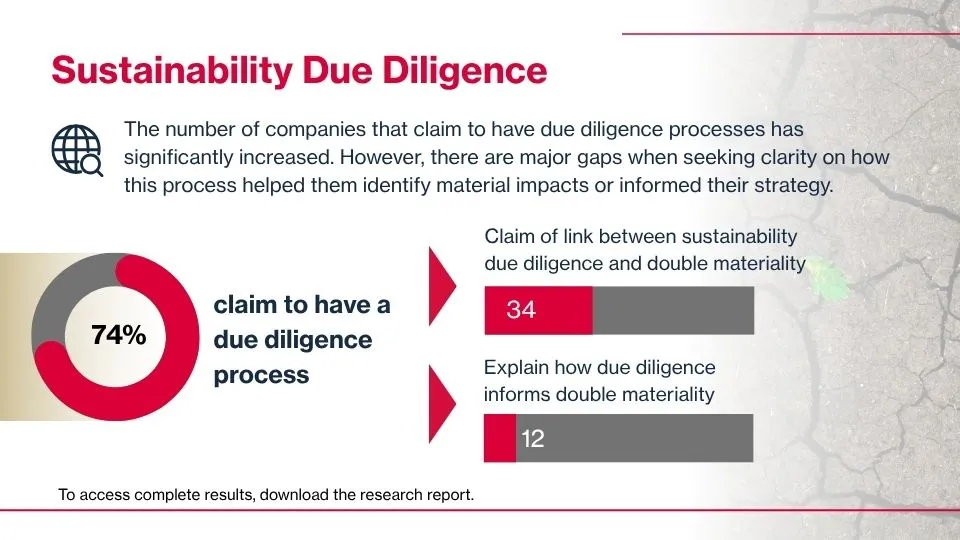

- Double materiality has quickly become a standard analytical lens, helping companies better understand how sustainability issues affect both their business and the world around them. The numbers underscore this point: while only 15% of companies described their impacts in 2024 in a similar research sample, 94% reported these in 2025. The number of those disclosing information on their due diligence process has also almost doubled.

These shifts mark a cultural change in corporate reporting, where sustainability disclosures are no longer a mere PR exercise but a strategic tool to understand critical challenges, from energy and resource use to climate uncertainty, value-chain resilience, and how companies manage them.

While the first year of CSRD implementation led to noticeable improvements, challenges remain.

- Critical elements to evaluate companies’ climate transition plans remain underreported, with only 15 out of 56 companies explaining how their plans may be jeopardised by dependencies in their business models, involving carbon intensive assets and products, or by external factors like market shifts, technological change, or new regulation. These 15 companies represent an important source of good practice.

- Gaps on key information regarding GHG Scope 3 data, with 15% of companies omitting Scope 3 categories typical for their sector, highlight the need for sector-specific guidance, not less. Additionally, disclosures on carbon removals and offsets remain limited and often lack methodological clarity.

- Even though many companies (85%) refer to their value chains, only 9 out of 100 clearly explain how they followed a risk-based approach, i.e. how they focus on specific activities, geographies or other factors leading to increased risks of sustainability impacts. Similarly, only 12 companies clearly explained how their due diligence process informs or is leveraged in their double materiality assessments. This indicates that many companies have followed a very cumbersome, yet unnecessary catch-all approach, instead of prioritising.

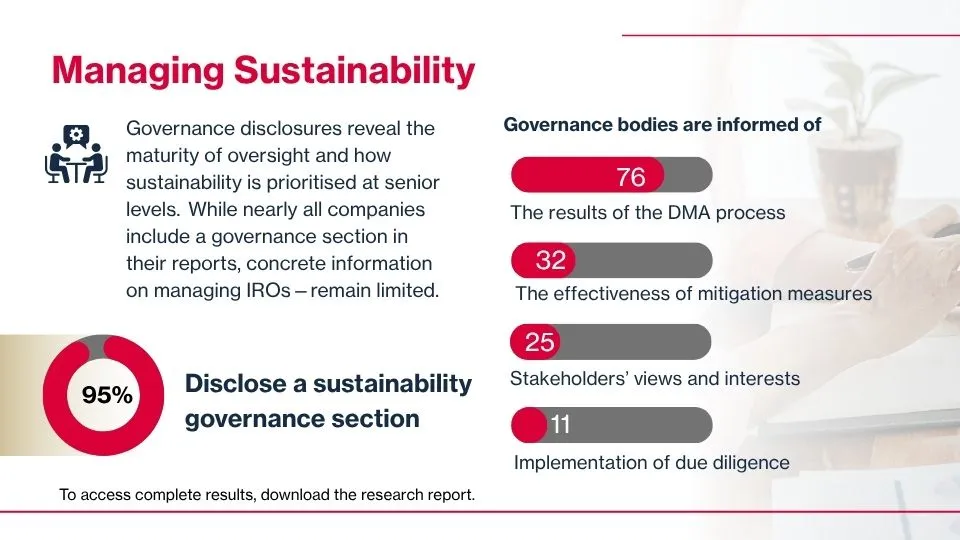

- Despite 95% of companies including a governance section in their reports, the information disclosed reveals major gaps in board-level awareness of the effectiveness of measures to address material impacts (32%), the implementation of due diligence (11%), or the perspectives of affected stakeholders (25%)

- While acknowledging shortcomings, the report also identifies areas for improvement within the ESRS. Notably, clearer requirements, methodologies, and sector-specific guidance could enhance consistency. Important points of attention include supply-chain transparency, quantification of financial effects, and biodiversity dependencies.

Particularly against the backdrop of the ongoing Omnibus simplification debate, such gaps and feedback underline why continued guidance—not deregulation—is essential to turn disclosure into effective risk management.

The research provides clear recommendations to policymakers and businesses on how to simplify reporting without weakening requirements, focusing on strategic and useful information.

The release of this report comes amid fierce discussions over the Omnibus simplification package and the rollback of corporate sustainability legislation. Proposals to dilute reporting and due diligence requirements risk undoing the progress achieved in just one reporting cycle. Misguided simplification efforts create uncertainty for companies that have already invested in improving their systems.

By limiting availability of critical data the EU will be compromising on its competitive edge. To scale up clean tech and advance EU's strategic goals in energy efficiency or resource autonomy, access to high-quality, large-scale data is essential. The CSRD secures this information flow from companies.

This is critical for the EU to strengthen industrial competitiveness, counter China’s lead in manufacturing and green tech, and withstand pressure from the U.S and other oil-rich countries to maintain dependence on fossil fuel imports.

As this report shows, reducing sustainability reporting to a compliance cost misses its value as a strategic asset for Europe’s industrial and geopolitical strength.

This publication was published by Frank Bold Society as part of a project funded by the European Climate Initiative (EUKI) of the German Federal Ministry for Economic Affairs and Climate Action (BMWK) to support the practical implementation of EU sustainability legislation by providing high quality, publicly available research and expert guidance.

Discover how European companies are managing ESG reporting. The new study by Frank Bold’s Responsible Companies team summarizes the first wave of sustainability reports from one hundred major European companies and shows that reporting under the CSRD provides valuable data for decision-making and is becoming an effective tool for risk management. Publication is part of the European Climate Initiative (EUKI) of the German Federal Ministry for Economic Affairs and Climate Action (BMWK).

Comprehensive Sustainability Report aligned with CSRD.

.webp)

A simplified ESG report for your business partners.

Mapped according to GHG Protocol Product Standard.

We are part of the Frank Bold Expert Group

Copyright ©

Aktuální rok script

Frank Bold